How to Stay Motivated When Paying Off Debt Takes Forever (Mindset + Milestones)

Paying off debt can feel like running on a treadmill: you’re working hard, but progress looks painfully slow. If you’ve ever thought, “This is taking forever,” you’re not failing—you’re experiencing the most common challenge in any debt-free journey: staying consistent when results are delayed.

The good news is that motivation isn’t something you either have or don’t have. It’s something you can build with the right systems, milestones, and mindset shifts. Here’s how to keep going—even when the finish line feels far away.

- Understand Why Motivation Fades (It’s Not Just “Willpower”)

- Turn a “Forever Goal” Into Short Milestones

- Use a Tracking System That Makes Progress Obvious

- Build a “Debt Payoff Routine” (So Motivation Isn’t Required)

- Set Up Micro-Rewards That Don’t Derail Your Budget

- Make Your Debt “Painful” in the Right Way

- Reduce Burnout With Sustainable Payments

- Stay Motivated When Life Throws You Off Track

- Keep Going—Future You Is Counting On It

Understand Why Motivation Fades (It’s Not Just “Willpower”)

Motivation typically drops for three reasons:

Progress feels invisible. Paying $300–$800/month can still look tiny compared to a big balance.

Life keeps happening. Emergencies, holidays, and stress make debt feel endless.

Your brain needs rewards. If you don’t create “wins” along the way, you burn out.

This is why relying on willpower alone is a trap. You need a plan that creates frequent, believable wins.

Turn a “Forever Goal” Into Short Milestones

A huge goal like “pay off $25,000” can be demoralizing because it’s too far away to feel real. Instead, create milestones that hit often enough to keep you engaged.

Try these milestone ideas:

Every $500 or $1,000 paid off (choose what feels meaningful)

Each debt paid off (even if it’s small)

Every 10% reduction in total balance

Interest rate wins (like refinancing, negotiating, or moving to a lower APR)

Then make those milestones visible. Put them on paper, in a notes app, or on a whiteboard where you’ll see them weekly.

Pro tip: If you’re using the debt snowball method, those early “paid off” wins can be incredibly motivating. If you’re using debt avalanche, build in milestone rewards since balances may drop more slowly at first.

Use a Tracking System That Makes Progress Obvious

If you don’t track progress in a way your brain can see, it’ll feel like nothing is happening.

Pick one of these simple tracking systems:

Debt payoff thermometer: Fill it in each month.

Balance snapshots: Record your total debt every payday or month-end.

A one-page debt dashboard: Total debt, minimum payments, payoff date estimate.

Visual chart (digital or paper): A line graph that trends down is powerful.

The goal isn’t perfection—it’s consistency. A simple tracker you actually use beats a fancy spreadsheet you avoid.

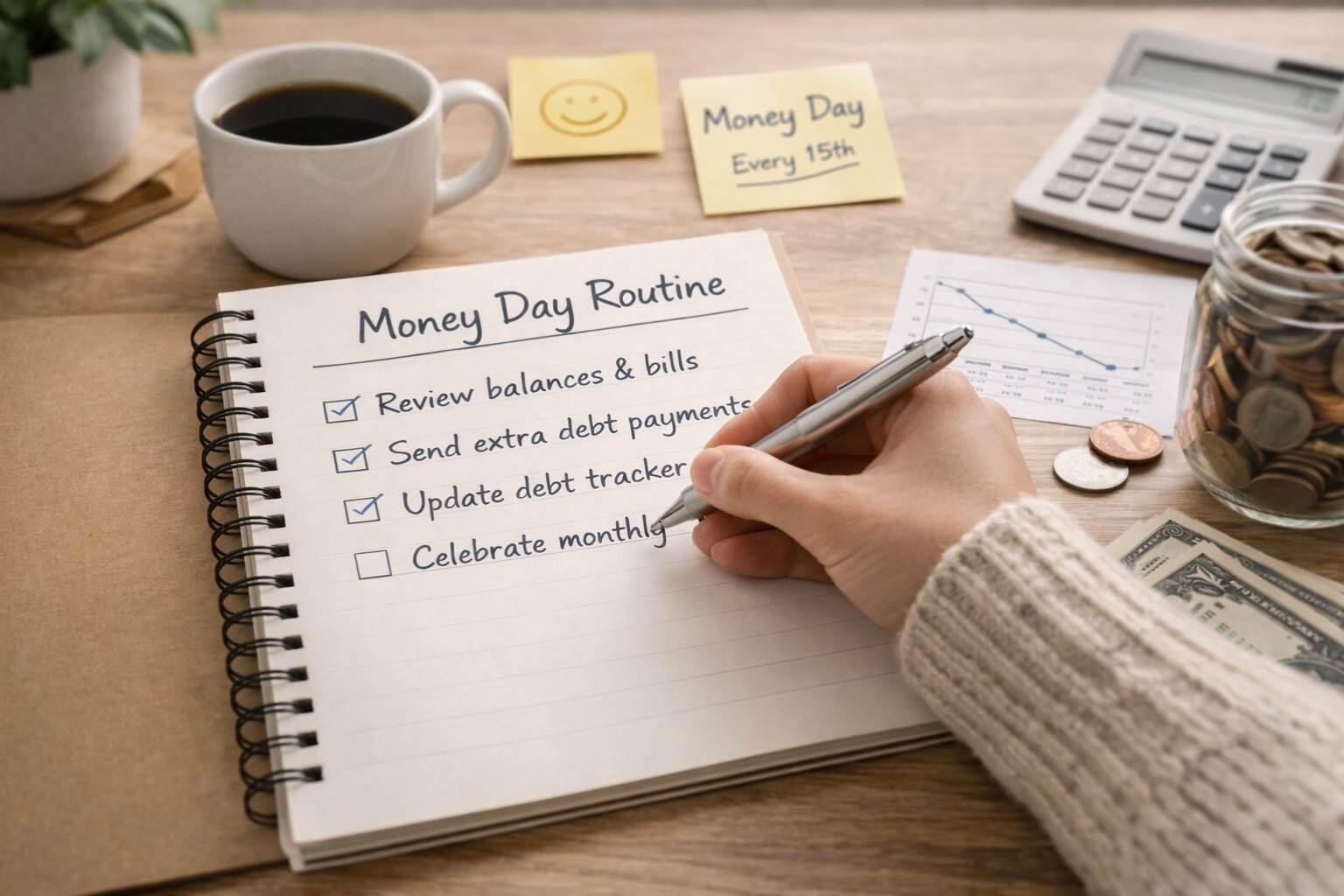

Build a “Debt Payoff Routine” (So Motivation Isn’t Required)

Motivation comes and goes. Routines stick.

Create a monthly routine you can repeat:

Pick a “money day” (same day each week or month)

Review your balances and upcoming bills

Send extra payments (even small ones)

Update your tracker

Write down one “win” from the month (yes, seriously)

When debt payoff is just “what you do on money day,” you stop negotiating with yourself.

Set Up Micro-Rewards That Don’t Derail Your Budget

You need rewards—but they must be budget-friendly, or you’ll sabotage progress.

Create a reward menu with “free” or low-cost options:

Movie night at home

Fancy coffee at home + a walk

Library book + cozy night in

A $10–$25 “fun fund” after a milestone

A friend's hangout that doesn’t revolve around spending

The key is to tie rewards to milestones, not emotions. Spending because you’re stressed makes debt feel worse. Spending because you hit a goal builds momentum.

Make Your Debt “Painful” in the Right Way

Sometimes you need a reminder of why you started—without spiraling into shame.

Try these motivation anchors:

Write a short “why” statement: “I’m paying off debt so I can ____.”

Keep a note of what debt costs you monthly in interest (even an estimate).

Create a simple vision board: debt-free life, goals, freedom, family, travel, etc.

This isn’t about guilt. It’s about staying connected to your real priorities when boredom hits.

Reduce Burnout With Sustainable Payments

A common reason people quit is that they set payments so aggressive they can’t live.

Watch for burnout signs:

Constantly “falling off” and restarting

Feeling resentful about your budget

Avoiding bank apps and statements

Using credit cards again to cope

If this is you, it may be time to adjust your plan:

Make sure you have a small buffer (even a starter emergency fund)

Allow a realistic spending category for fun/social life

Choose an extra payment amount you can maintain for 6–12 months

Consistency beats intensity in long debt journeys.

Stay Motivated When Life Throws You Off Track

Setbacks don’t mean you failed—they mean you’re human.

If you have a rough month:

Pay the minimums and protect necessities

Rebuild your next month’s plan

Restart extra payments ASAP, even if it’s small

Focus on the next best step, not the “perfect” plan

A helpful mindset shift: Your plan doesn’t need to be perfect. It needs to be restartable.

Keep Going—Future You Is Counting On It

Debt payoff is one of the most emotionally demanding money goals because the reward is delayed. But every payment you make is proof you’re changing your financial future. Build milestones, track progress visually, and create routines that don’t rely on willpower.

Your next step: pick one tracking method and one milestone to celebrate this month—and make it visible today.

More tips for your financial journey